Europe Endodontic Reparative Cement Market Overview - Definition, scope, and significance?

The Europe Endodontic Reparative Cement market comprises products used to seal and repair root canals, restore dentinal structures, and line cavities in therapeutic dental procedures. These cements are essential for achieving hermetic seals, preventing microbial leakage, and supporting tissue healing. The market’s scope spans hospitals, dental clinics, and ambulatory surgical centers across European nations, reflecting the growing emphasis on advanced endodontic care and long‑term tooth preservation.

Europe Endodontic Reparative Cement Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include rising prevalence of dental diseases, increasing demand for minimally invasive procedures, and strong reimbursement frameworks in many European health systems. Technological advances such as bioceramic sealers enhance clinical outcomes, creating further demand. Restraints arise from stringent regulatory approvals and high product costs, which can limit adoption in price‑sensitive settings. Challenges involve supply‑chain disruptions and the need for ongoing clinician education. Opportunities exist in expanding indications, developing bioactive formulations, and leveraging digital dentistry integrations.

Europe Endodontic Reparative Cement Market Growth Trends - Current and emerging trends shaping the market?

Current trends show a shift toward bioceramic‑based sealers due to their superior biocompatibility and sealing ability. Clinicians are increasingly preferring single‑cone techniques that rely on advanced cements. Emerging trends include incorporation of nanomaterials to improve mechanical strength, and the adoption of chair‑side dispensing systems that streamline workflow. Sustainability considerations are prompting manufacturers to explore eco‑friendly packaging and reduced‑toxicity formulations.

COVID-19 Impact on the Europe Endodontic Reparative Cement Market - Pandemic effects and recovery trajectory?

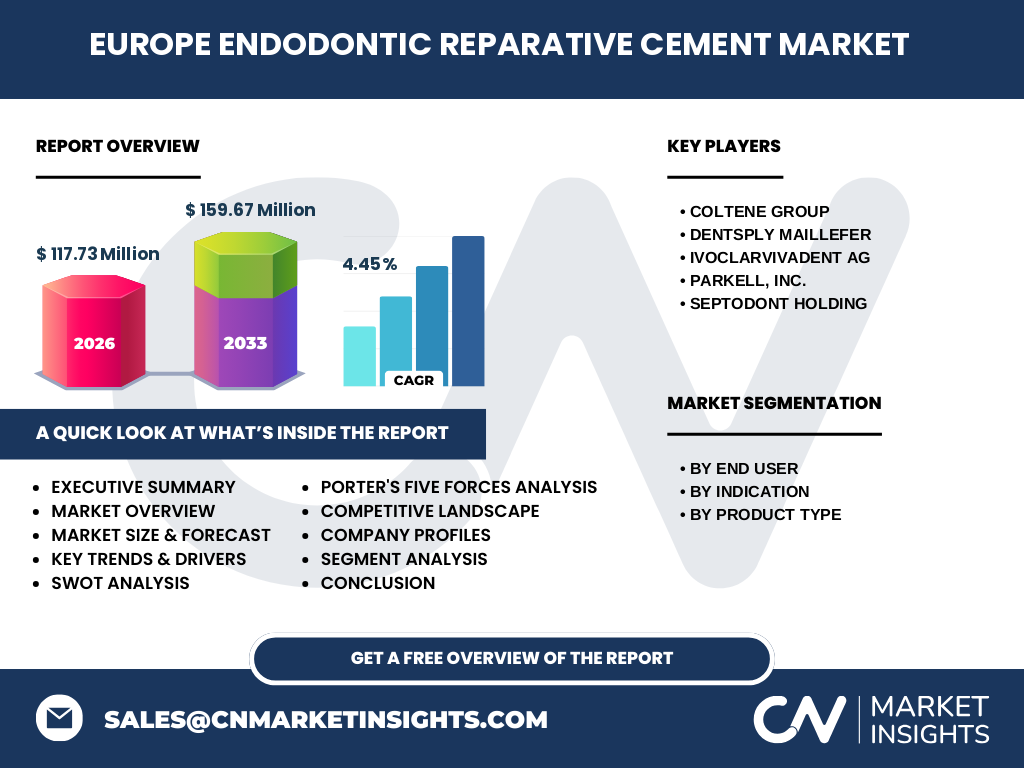

The COVID‑19 pandemic caused temporary clinic closures and reduced elective dental visits, leading to a short‑term dip in cement consumption. However, heightened awareness of oral health and rapid resumption of services have driven a strong rebound. Recovery is evident in the projected CAGR of 4.45%, indicating that post‑pandemic demand is not only restored but also accelerating as patient backlogs are addressed.

Europe Endodontic Reparative Cement Market Competitive Landscape - Major competitors and market consolidation?

The competitive arena is led by established dental manufacturers such as Coltene Group, Dentsply Maillefer, Ivoclar Vivadent AG, Parkell, Inc., and Septodont Holding. These players compete on product innovation, clinical evidence, and distribution reach. Recent years have seen strategic acquisitions and partnership agreements aimed at broadening product portfolios and enhancing market penetration, signaling moderate consolidation within the sector.

Executive Summary - High-level overview and key findings about Europe Endodontic Reparative Cement Market?

The European market is valued at €117.73 million in 2026 and is projected to reach €159.67 million by 2033, reflecting a CAGR of 4.45%. Growth is propelled by expanding end‑user bases, especially dental clinics, and a clear preference for bioceramic‑based sealers. While regulatory complexity and cost remain constraints, opportunities in novel bioactive products and digital integration present strong upside potential for investors and manufacturers.

Europe Endodontic Reparative Cement Market Forecast - Projections for 2025-2032 period?

Based on the current trajectory, the market is expected to maintain steady expansion through 2032, staying in line with the 4.45% CAGR. Incremental growth will be supported by continued adoption of advanced cement types and rising procedural volumes in both hospital and private clinic settings. The forecast underscores a robust outlook, positioning the market as a valuable segment for long‑term strategic planning.

Europe Endodontic Reparative Cement Market Size and Share by Segmentation - Breakdown by segment?

Segmentation by end‑user shows hospitals, dental clinics, and ambulatory surgical centers each contributing distinct demand patterns, with dental clinics typically representing the largest share due to high patient turnover. Indication‑wise, root canal obturation commands the primary share, followed by dental restoration and cavity lining. Product‑type distribution highlights bioceramic‑based sealers as the fastest‑growing category, while zinc oxide eugenol‑based and epoxy resin‑based cements retain solid market positions, and calcium‑hydroxide based variants serve niche applications.

Global Europe Endodontic Reparative Cement Market Size and Share by Region - Geographic distribution?

Within Europe, market activity is concentrated in Western and Central countries where advanced dental infrastructure and reimbursement support are strongest. Northern Europe contributes a notable share due to high public health expenditure, while Southern regions display growing demand driven by expanding private dental networks. The overall European share reflects a balanced distribution across these sub‑regions, aligning with the continent’s diverse healthcare landscapes.

Regional Analysis of the Europe Endodontic Reparative Cement Market - Detailed regional market performance?

Western Europe, led by Germany, France, and the United Kingdom, exhibits the highest consumption levels, driven by large hospital networks and premium dental practices. Central Europe, including Austria, Switzerland, and the Benelux states, shows steady growth correlated with strong regulatory frameworks. In Eastern Europe, emerging markets are adopting modern endodontic techniques, indicating untapped potential. Each region’s performance is influenced by local clinical guidelines, reimbursement rates, and practitioner training programs.

Leading Company Profiles in the Europe Endodontic Reparative Cement Market - Industry players and strategies?

Coltene Group focuses on expanding its bioceramic portfolio and strengthening distribution partnerships across EU nations. Dentsply Maillefer leverages extensive clinical research to validate product efficacy, targeting high‑volume dental chains. Ivoclar Vivadent AG emphasizes premium, aesthetically driven cement solutions for restorative indications. Parkell, Inc. differentiates through cost‑competitive offerings for ambulatory surgical centers. Septodont Holding invests in R&D for novel calcium‑hydroxide formulations and pursues strategic collaborations with academic institutions.

Porter's Five Forces Analysis of the Europe Endodontic Reparative Cement Market - Competitive forces assessment?

Threat of new entrants remains moderate due to high regulatory barriers and required R&D investment. Bargaining power of buyers is elevated as large dental networks negotiate pricing and demand product differentiation. Bargaining power of suppliers is low to moderate; raw material sources are relatively standardized. Threat of substitutes is limited, as alternative materials lack the sealing performance of dedicated reparative cements. Industry rivalry is strong, driven by product innovation and brand loyalty among clinicians.

SWOT Analysis of the Europe Endodontic Reparative Cement Market - Strengths, weaknesses, opportunities, threats?

Strengths: Advanced clinical efficacy, growing adoption of bioceramic technology, and robust reimbursement environments.

Weaknesses: High product cost, complex regulatory pathways, and uneven market education.

Opportunities: Development of bioactive and nanostructured cements, expansion into emerging European markets, and integration with digital workflow platforms.

Threats: Price pressure from generic alternatives, potential supply chain disruptions, and evolving regulatory standards.

Europe Endodontic Reparative Cement Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with raw material suppliers (e.g., calcium silicates, polymers), progresses to R&D and formulation centers, then to manufacturing facilities with strict quality controls. Distribution channels include wholesale distributors, direct sales to hospital procurement offices, and dental practice supply chains. End‑users—clinicians in hospitals, dental clinics, and ambulatory centers—provide feedback that loops back to product development, completing the cycle.

Key Investment Insights in the Europe Endodontic Reparative Cement Market - Strategic investment recommendations?

Investors should prioritize companies with strong bioceramic pipelines and proven clinical data, as these segments exhibit the highest growth momentum. Partnerships with academic research groups can accelerate innovation and market entry. Diversifying across end‑user segments, especially targeting ambulatory surgical centers, can mitigate concentration risk. Monitoring regulatory updates in major European markets will be essential for timing capital allocation.

Europe Endodontic Reparative Cement Market Conclusion - Summary and key takeaways?

The market demonstrates a healthy growth trajectory, underpinned by a 4.45% CAGR and a projected increase from €117.73 million to €159.67 million by 2033. Bioceramic‑based sealers are reshaping clinical practice, while hospitals and dental clinics remain the primary demand engines. Despite cost and regulatory challenges, the market offers compelling opportunities for product innovation, regional expansion, and strategic investment.

Research Methodology - How this research was conducted?

The study employed a mixed‑method approach, combining primary interviews with key opinion leaders, dental practitioners, and supply‑chain executives, alongside secondary data extraction from industry reports, regulatory databases, and company publications. Market sizing utilized a top‑down approach anchored to the provided 2026 base value, with forecasts derived through compound annual growth rate calculations and trend extrapolation.

Research Scope - Coverage and limitations?

The scope covers the European endodontic reparative cement market, segmenting by end‑user, indication, and product type. Geographic focus is confined to European nations, excluding non‑European regions. While the analysis integrates the latest available data, it does not quantify market shares for individual companies beyond the qualitative insights presented, and the forecast assumes stable economic conditions across the projection horizon.

Key Companies and Recent Developments in the Europe Endodontic Reparative Cement Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Coltene Group recently launched a next‑generation bioceramic sealer with enhanced radiopacity, partnering with several university dentistry departments for clinical trials. Dentsply Maillefer announced a strategic acquisition of a niche calcium‑hydroxide cement line to broaden its product suite. Ivoclar Vivadent AG introduced a premium, shade‑matched reparative cement designed for aesthetic restorations. Parkell, Inc. released a cost‑effective epoxy resin based cement targeting ambulatory surgical centers. Septodont Holding entered a joint‑development agreement with a biotech firm to explore bioactive additives for improved tissue regeneration.